One of the most important factors to understand when buying a home is your loan-to-value ratio (LVR). It’s a measure lenders use to assess how risky it is to lend you money, based on the size of your loan compared to the value of the property you’re buying.

Whether you’re a first-home buyer or a seasoned investor, understanding your LVR can help you make more confident decisions — from how much deposit or equity you’ll need to the interest rate you’re offered.

In this guide, we’ll break down what LVR means, why it matters, and how it can impact your home loan.

Reviewed by the OurTop10 Research Team | Last updated: April 2026

What is LVR?

Loan-to-value ratio (LVR) is the size of your mortgage compared to the value of the property you’re buying, shown as a percentage. Lenders use LVR to assess how risky it is to lend to you — the larger your loan relative to the property (i.e. the higher your LVR), the higher the risk.

What is a good LVR?

Generally, a good LVR is considered to be 80% or lower — it puts you in a stronger position as a borrower because you’re borrowing a smaller share of the property’s value. This reduces the risk to the lender, which means you may qualify for a better interest rate and avoid having to pay Lenders Mortgage Insurance (LMI).

On the flip side, a higher LVR (above 80%) means you’re borrowing a larger portion of the property’s value, which increases the lender’s risk and can result in a higher interest rate and LMI being added to your costs.

You should know: LMI is generally applicable to loans with an LVR above 80% to protect the lender (not you) in case you’re unable to repay the loan. LMI can either be paid upfront or rolled into your loan.

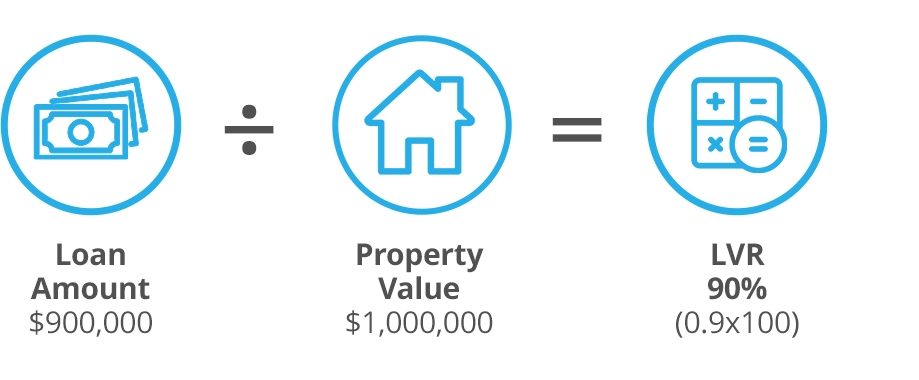

How do you calculate LVR?

The formula to calculate LVR is simple: LVR = (Loan amount ÷ property Value) × 100

For example, if you’re buying a property worth $1,000,000 and borrowing $900,000 (meaning you have a $100,000 deposit, or 10%), your LVR would be:

LVR = ($900,000 loan ÷ $1,000,000 property value) × 100 = 90% LVR

Important: When calculating LVR, the property value isn’t always the purchase price. Lenders use their own valuation, which may be higher or lower than what you paid and this can affect your final LVR.

LVR on a $1,000,000 Property

Your loan-to-value ratio can vary depending on the size of your home loan and your deposit. Here’s a quick breakdown of how different deposit amounts/equity translate into LVRs:

|

Loan amount |

Deposit/equity |

LVR |

|

$1,000,000 |

$50,000 |

95% |

|

$1,000,000 |

$100,000 |

90% |

|

$1,000,000 |

$200,000 |

80% |

|

$1,000,000 |

$300,000 |

70% |

|

$1,000,000 |

$400,000 |

60% |

|

$1,000,000 |

$500,000 |

50% |

How lenders use LVR to calculate your interest rate & borrowing power

Every lender and mortgage broker will look at your LVR when you apply for a home loan — whether you’re buying a property or refinancing an existing one. Your LVR is one of the key factors used to determine how much you can borrow and your interest rate.

Impact of LVR on your mortgage approval

Your LVR is one of the main factors in whether your home loan gets approved and on what terms. Lenders use it to assess risk, alongside factors like your income, expenses, credit history, and employment. A lower LVR generally strengthens your application, while a higher LVR can make approval more challenging (but not impossible). You may face stricter lending criteria, need to provide more supporting documentation or be limited to fewer lenders.

In some cases, lenders may decline your home loan application altogether if the risk (your LVR) is considered too high.

Most lenders in Australia will only lend up to 95% of a property’s value (your LVR), meaning you’ll need at least a 5% deposit or equity to be approved. If LMI is required, it can often be added to the loan, pushing your total loan amount to around 97%–98% of the property’s value.

How your LVR affect your borrowing capacity

Your LVR also affects how much you can borrow for a home loan. For example, if a lender caps lending at 80% LVR and you’re buying a $1,000,000 property, you can only borrow up to $800,000. You’d then need to cover the remaining $200,000 as a cash deposit or usable equity from another property.

But if the lender caps lending at 95% LVR, you could borrow up to $950,000, reducing your required deposit or equity to $50,000, although LMI would likely apply, unless you qualify for an LMI waiver.

Interest Rates and LVR

The LVR doesn’t just affect the amount you can borrow. Most lenders adjust interest rates based on the LVR as well. Usually, a lower LVR means a lower interest rate. Conversely, a higher LVR can lead to higher interest rates, as the lender wants to cover the extra risk. So, the lower your LVR, the bigger your deposit and the better your loan conditions will likely be.

How lenders use LVR to calculate your interest rate

Lenders use your LVR as a key pricing tool when determining your interest rate. Borrowers with lower LVRs (e.g. 60% or below) typically receive the most competitive rates, while those with higher LVRs (closer to 80%) will pay slightly more.

Even small differences in LVR can lead to noticeable changes in both interest and comparison rates, which can add up over the life of the loan. For example, current rates from CommBank show a difference of around 0.45 percentage points between borrowers with an LVR of 60% or less (6.09% p.a.) and those in the 80–90% range (6.54% p.a.).

4 ways to lower your LVR

- Increase your deposit: The larger your deposit, the lower your LVR. Saving more may take extra time, but it could save you thousands over the life of your loan through a lower interest rate and avoiding LMI.

- Get help from family: This could be a cash gift towards your deposit or a guarantor loan — where a family member (often a parent) uses their property as security. Both options can help reduce your LVR and improve your loan terms.

- Buy a cheaper property: Choosing a more affordable property can reduce your LVR and make it easier to secure a loan. It doesn’t mean giving up on your dream — a smaller or simpler home can still tick the boxes (and often comes with lower upkeep costs).

- Use government grants or incentives: If you’re a first-home buyer, explore schemes like the First Home Owner Grant (FHOG) and the First Home Guarantee (FHBG). The FHOG is a cash grant available through your state or territory for eligible buyers, while the FHBG allows you to purchase a property with as little as a 5% deposit without paying LMI.

LVR when buying an investment property

Lenders usually require a lower LVR (70-80% or less) for investment properties than for homes you plan to live in. That’s because investment loans are seen as higher risk, as they often rely on rental income, which can be less predictable than personal income.

As a result, many lenders require a larger deposit or equity contribution for investment loans. They may also charge higher interest rates to account for the added risk. However, LVR limits can vary between lenders, and some may still offer relatively higher LVRs for investment properties if you have a strong financial position.

Risks of using a high LVR for property investment

While a low LVR is generally ideal for owner-occupiers, some property investors are more comfortable with a higher LVR. This is because they may choose to contribute less equity or cash towards each purchase. This allows them to grow their portfolio faster without needing to wait for property A to increase in value or build sufficient equity before purchasing property B and C.

The downside is that this strategy comes with risks, including:

- Market volatility: If property values fall, your LVR could rise — potentially leaving you owing more on your mortgage than the property is worth (known as negative equity).

- Higher costs: Loans with higher LVRs often come with higher interest rates to offset the risk to the lender. They may also face additional fees and stricter lending conditions.

- Regulatory changes: Changes to lending rules can impact LVR limits and borrowing conditions. If regulations tighten, it may become harder to secure finance or refinance, especially with a higher LVR.

LVR and postcode restrictions

Some lenders may cap the LVR on home loans based on the property’s suburb or postcode. This is because certain areas are considered higher risk — for example, high-density apartment markets in Sydney, where there may be an oversupply of similar properties or lower resale demand.

It’s important to check this with a lender or your broker, so you understand how much deposit you’ll need and can plan accordingly.

You’ll find the best Sydney mortgage brokers, Melbourne mortgage brokers, and Brisbane mortgage brokers in OurTop rankings to help guide you through complexities.

FAQs about Loan-To-Value Ratio (LVR)

-

What isn’t included in the loan amount when calculating LVR?

Banks use either a market valuation or a bank valuation to assess your property’s value. A market valuation is an estimated sale price based on comparable properties in the area, often derived from platforms like RP Data and internal databases. A bank valuation, on the other hand, is carried out by a licensed valuer on behalf of the lender and is typically more conservative. Lenders will typically use the lower of the two values to calculate your LVR.

-

What isn’t included in the loan amount when calculating LVR?

Upfront costs like conveyancing fees, loan setup costs, mortgage registration fees and stamp duty are excluded from your loan amount when lenders calculate your LVR.

-

Do I need a good LVR when refinancing?

Yes — your loan-to-value ratio still matters when refinancing. Lenders assess any refinance application like a new loan, and your LVR will affect your rate and approval conditions. You’ll need at least 20% equity (an LVR of 80% or lower) to avoid potentially paying LMI again.