Refinancing your home loan is one of the most significant financial moves you can make as a homeowner. But knowing when to refinance your mortgage is where most people get stuck. Refinance too early, and you might cop break fees that wipe out any savings. Leave it too long, and you could be paying thousands more than you need to each year.

This guide walks you through the five clearest signals that it’s time to take a fresh look at your loan and what to do when you spot them.

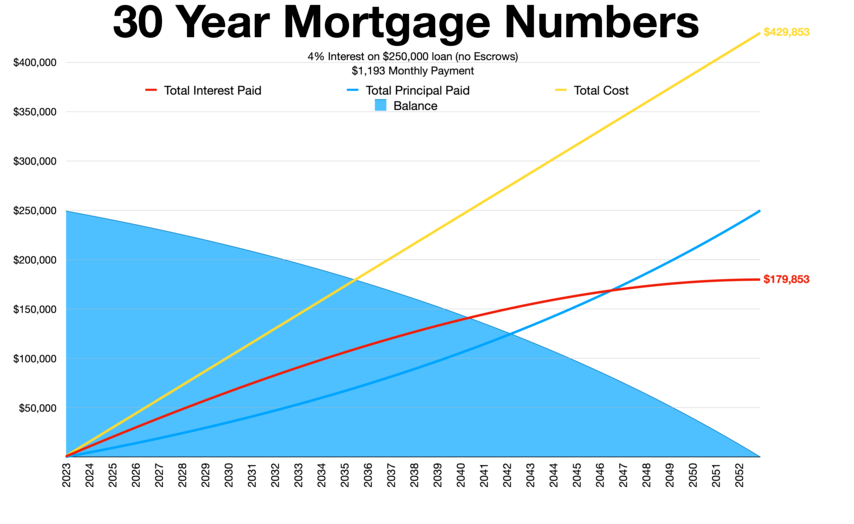

How home loan repayments work

When you take out a home loan, your repayments are made up of two parts: the principal (the amount you borrowed) and the interest charged by the lender on that balance. In the early years of a loan, a larger portion of each repayment goes towards interest rather than paying down the actual debt. Over time, as the principal reduces, more of each payment chips away at what you owe.

Want to see how your repayments break down? Try our free Home Loan Repayment Calculator.

What does refinancing actually mean?

Refinancing simply means replacing your existing home loan with a new one, either with your current lender or a different one. You’re essentially paying out your old loan and starting fresh under new terms.

The new loan might have a lower interest rate, different features, a new loan term or a contrasting loan structure altogether. You might also be able to consolidate other debts into the loan, access equity you’ve built up or switch from a variable to a fixed rate (or vice versa).

It’s a normal part of managing your mortgage over time, and something a good mortgage broker will proactively flag for you rather than leaving you to figure out on your own.

Wondering if the numbers stack up for you? Our Refinancing Calculator can give you a quick estimate.

5 signs it might be time to refinance your mortgage

There’s no single moment that works for everyone, but there are some clear patterns that consistently signal it’s worth reviewing your loan. Here’s what to look for.

Sign 1 — Interest rates have dropped by 0.5% or more

This is the most straightforward trigger. If the market has shifted and home loan rates are sitting notably lower than what you’re currently paying, the maths often stack up in favour of switching.

A drop of 0.5% or more is generally the threshold where the savings start to outweigh the costs involved in refinancing, such as discharge fees, application fees and any settlement costs. Below that, it can be a closer call.

In 2026, with lenders actively competing for business and further rate movements expected from the Reserve Bank of Australia, it’s worth getting a comparison done even if you haven’t looked in 12 months.

What could help: Ask a mortgage broker to run a side-by-side comparison of your current rate against what’s available today. Make sure any comparison accounts for the full cost of switching, not just the headline rate.

Sign 2 — Your property’s value has grown and your equity is above 20%

As your property increases in value, your loan-to-value ratio (LVR) improves. LVR is simply how much you owe compared to what the property is worth. A lower LVR puts you in a stronger borrowing position because the lender’s risk is reduced.

Once your equity clears 20% (meaning your LVR drops below 80%), two things happen: you’re no longer required to pay Lenders Mortgage Insurance (LMI), and you become eligible for more competitive interest rates. If you bought with a smaller deposit and have been paying down the loan while property values rose, you may have quietly crossed this threshold without realising it.

What could help: Get an updated property valuation. Many brokers can arrange an indicative valuation at no cost. If your equity has grown enough to shift your LVR into a better band, refinancing could unlock a lower rate and better loan conditions.

Sign 3 — Your credit score has improved significantly

Your credit profile when you first took out the loan isn’t necessarily where it sits today. If you’ve paid down debts, cleared credit cards, fixed past defaults or simply built a strong repayment history over several years, your credit score may have improved considerably.

Lenders price risk, and a better credit profile makes you a lower-risk borrower. That can translate directly into access to sharper rates and a wider range of products you may not have qualified for when you originally applied.

What could help: Checking your credit score is a good starting point — MoneySmart outlines what factors influence your score and how to access your report for free. If there’s been a meaningful improvement, it’s worth having a broker assess what you’d now qualify for compared to your current terms.

Sign 4 — Your fixed rate period is about to end

Fixed-rate loans offer certainty, but they come with a built-in expiry. When your fixed term ends, most lenders roll you onto what’s known as a revert rate, which is typically their standard variable rate. In many cases, this revert rate is not competitive.

The window just before your fixed term ends is one of the most critical moments to act. If you don’t take steps to refinance or negotiate a new rate, you could find yourself automatically moved onto a higher rate with no fanfare from the lender.

What could help: Check your loan documents for the exact end date of your fixed term. Start the refinancing process at least 60 to 90 days before that date — this gives enough time to compare options, submit an application and have everything settled before the revert rate kicks in.

Sign 5 — Your life circumstances have changed

A loan that made sense when you signed it may not suit your situation today. Life changes, and your mortgage should keep pace.

Common changes that prompt a refinancing review include:

- Getting married or separating, which may change your borrowing capacity or how the loan is structured

- Having children and moving to a single income, making lower repayments or an offset account more valuable

- A significant increase in income that opens up faster repayment strategies

- Wanting to access equity to fund a renovation, investment property or other goal

- Simply wanting a loan structure that better suits how you manage money now

None of these requires a financial crisis to justify a review. Refinancing can be proactive, not reactive. The best mortgage for you three years ago is rarely the best one for you today.

What could help: Sit down with a mortgage broker and walk through how your circumstances have changed. A good broker won’t just look at your interest rate. They’ll look at the full picture and find a loan structure that fits where your life is heading.

A few things to watch before you refinance

Not every situation that looks like a good refinancing opportunity actually is. There are a few things worth checking before you commit.

- Break costs on fixed loans — If you’re still inside a fixed rate period and want to refinance early, your lender may charge a break fee. These can sometimes be significant, so it’s worth calculating whether the savings from the new loan outweigh the cost of exiting the old one early.

- The true cost of switching — Look beyond the interest rate. Discharge fees, application fees, settlement costs and annual fees on the new loan all factor in. A broker can put together a net savings figure so you’re comparing apples with apples.

How long you plan to stay in the property — If you’re planning to sell within the next year or two, the benefits of refinancing your home loan may not materialise in time to be worthwhile.