How income annualisation works

Income annualisation is actually a simple calculation:

Income earned so far ÷ number of days or pay periods worked × 12 months

However, lenders rarely stop there.

In practice, banks apply additional filters to manage risk and meet responsible lending requirements. This may include averaging income over a longer timeframe, excluding short-term spikes that are unlikely to repeat, applying shading to variable components or placing caps on certain income types altogether.

Adjustment type | What it means in practice | Why lenders apply it |

Averaging | Income is averaged over a longer period, such as 6, 12 or 24 months | To smooth out fluctuations and reduce reliance on recent spikes |

Shading | A percentage of variable income is reduced, often by 20 to 50% | To allow for income volatility and uncertainty |

Exclusion | Certain income components are excluded entirely | When income is irregular, one-off or not ongoing |

Capping | Income is limited to a maximum amount | To prevent unusually high short-term earnings from overstating capacity |

History requirements | Income is only included after a minimum timeframe | To confirm consistency and stability |

According to guidance from the Australian Prudential Regulation Authority (APRA) and major bank credit policies, conservative treatment of non-guaranteed income is a core risk control. Lenders are required to assess whether income is sustainable over the life of the loan, not just whether it has been earned recently.

How different incomes types are annualised

Different income streams are treated differently. Understanding these distinctions is essential to setting realistic borrowing power expectations.

Base salary

Base income is the simplest to assess. If you’re employed on a permanent full-time or part-time basis, lenders generally accept your current base salary once it is verified by payslips and an employment contract.

Annualisation may still apply if you started mid-year or recently received a pay rise. In those cases, banks often annualise the new rate but may request confirmation from your employer to ensure the income is ongoing.

Overtime income

Overtime is rarely included at 100 per cent.

Most lenders require a consistent history and will review overtime earned over six to 12 months rather than projecting a recent high period forward. Even when overtime feels reliable, banks commonly reduce the final figure to account for variability.

Bonuses and commission

Bonuses and commissions are assessed conservatively. Lenders usually want to see a minimum history of six to 24 months and will often average earnings across multiple years.

One-off bonuses are commonly excluded, and even when income is trending upward, some lenders will rely on the lower historical average rather than the most recent figure. This creates one of the largest gaps between what borrowers earn and what banks assess.

Casual and contract income

Casual and contract income can be annualised, but evidence is critical.

Lenders typically look for consistent income over at least six to 12 months, regular hours or contracts and continuity within the same industry. Where hours fluctuate significantly, banks often rely on averaging rather than projecting the latest payslip.

Some lenders will not annualise casual income at all until a minimum timeframe has been met.

Self-employed income

Self-employed income is rarely annualised from payslips alone. Most lenders rely primarily on tax returns, notices of assessment and business financials.

Year-to-date figures may be considered in limited cases, but they’re usually heavily adjusted and used alongside historical income.

Using annualised income calculators correctly

An annualised income calculator provides a starting point for estimating borrowing capacity. While it doesn’t reflect a lender’s final decision when granting a loan, it’s a useful tool for early planning and setting realistic expectations.

To get the most accurate result, the information entered must reflect what lenders actually assess.

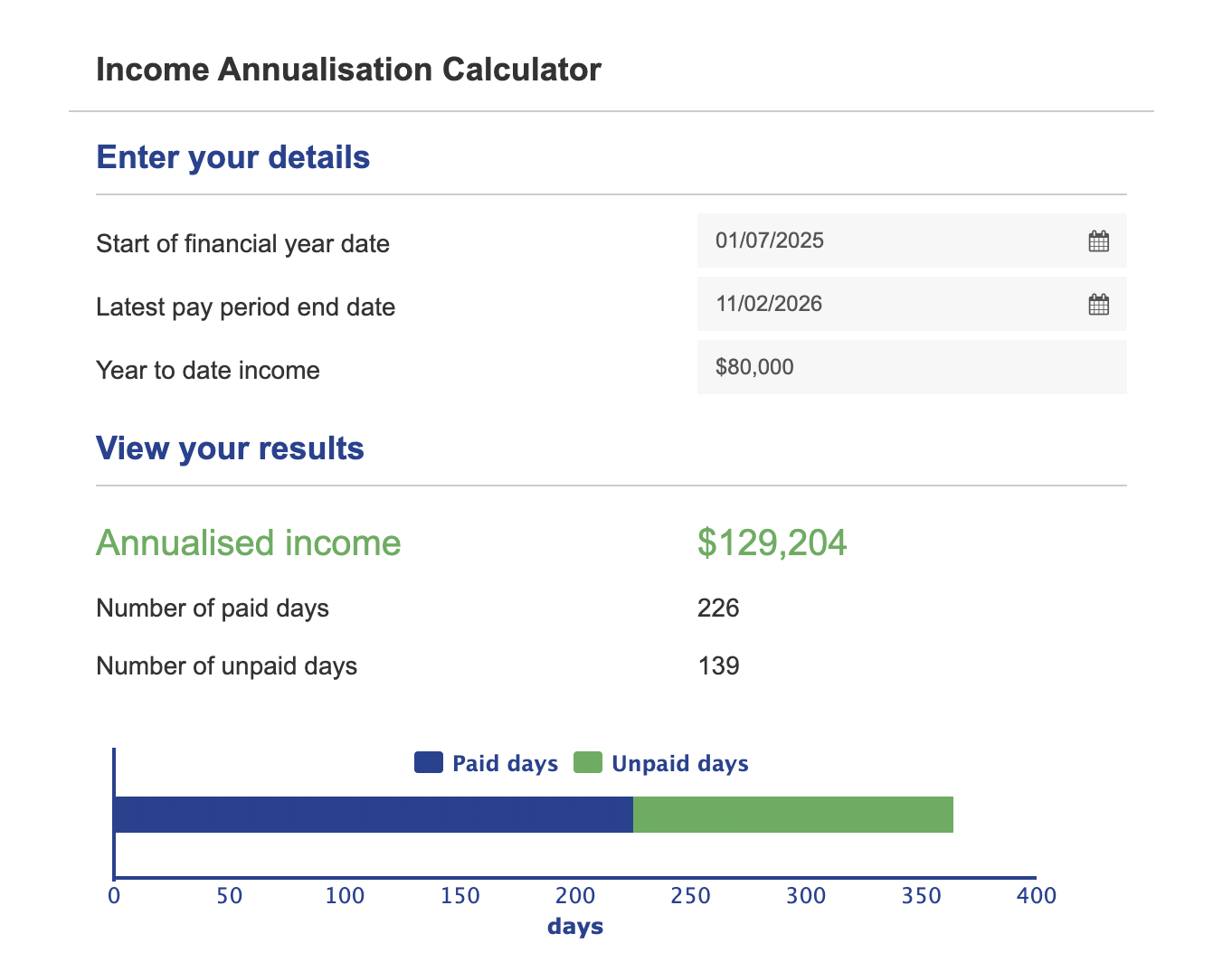

What figures to enter

Our income annualisation calculator asks for three key details:

Start of the financial year date

Latest pay period end date

Year-to-date gross income

These inputs allow the calculator to determine how much income has been earned over the paid portion of the year, then project that pace across a full 12-month period.

When this calculator is most useful

This calculator is most accurate when:

Income has already been paid and appears in year-to-date total.

The borrower is partway through the financial year.

Earnings have been reasonably consistent over that period.

For income types such as bonuses, overtime or casual work, the calculator can only annualise what has already been earned. It does not determine how much of that income a lender will ultimately accept.

Worked example

Assume a borrower earns variable income and enters the following details into the calculator:

Start of financial year: 1 July

Latest pay period end date: 31 January

Year-to-date gross income: $48,000

Based on the number of paid days between 1 July and 31 January, the calculator projects the income across a full year. In this example, the result produces an annualised income of approximately $81,448.

From here, a lender would still assess how that income is structured, including whether any portion is variable, discretionary or subject to shading.

Why broker guidance matters

According to The Value of Mortgage and Finance Broking 2025 report by Deloitte and the Mortgage & Finance Association of Australia Value of Mortgage and Finance Broking, 75 per cent of new residential home loans are now arranged through mortgage brokers. A key reason is the growing complexity of income assessment, particularly for borrowers with variable or non-standard income.

A mortgage broker can take the calculator result and assess it against real lender policy. This includes identifying which lenders are more favourable for your income type, how much of your income is likely to be accepted and whether any adjustments are likely to apply before you submit an application.

This step is especially important if you are buying property, seeking pre-approval or making offers based on a borrowing power estimate.

Speak to a mortgage broker for a lender-accurate assessment

Income annualisation is a standard part of modern home loan assessments, particularly when income is irregular or only part of the financial year is available.

While the calculation itself is straightforward, lender adjustments such as shading, averaging and income caps can significantly affect the final assessable income.

If you would like a lender-accurate view of your income, you can speak with a mortgage broker through OurTop10 to understand how your income is likely to be considered by lenders before you apply.

For more tools and guides to help you understand borrowing power, income assessment and property lending, visit our blog.