Introduction

Sometimes, the homebuying journey feels like it needs a dictionary. There are so many new terms to get your head around. One of those terms is loan-to-value ratio, or LVR. It might sound confusing, but understanding LVR is easier than you think. Simply put, the term LVR is a tool banks use to figure out how risky it is to lend you money for a home. Don’t forget, the best way to get a precise LVR for your specific scenario is from a top-rated Sydney mortgage broker.

Whether you’re a first-time buyer or a seasoned property investor, understanding LVR helps you make smarter decisions about your mortgage. In this article, we’ll break down what LVR means, why it matters, and how it impacts you when buying a home.

What Is LVR and How Do You Calculate It?

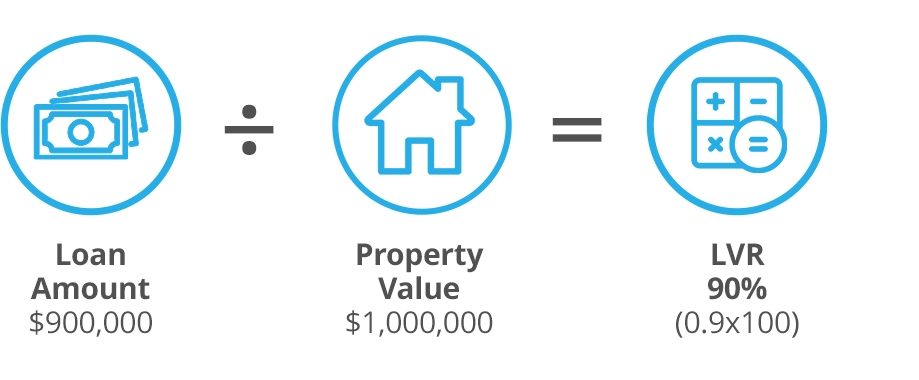

LVR, or Loan-to-Value Ratio, is a percentage that compares the valuation ratio of your home loan to the value of the property you’re buying. The formula to calculate LVR is simple:

LVR = (Loan Amount/Property Value) × 100

For instance, if you’re buying a property worth $500,000 with a loan amount of $400,000, your LVR would be:

LVR = (400,000 / 500,000) × 100 = 80% LVR

Important: When calculating LVR, the property’s value doesn’t necessarily mean the sale price. It’s determined by the bank’s valuation, which might differ from what you paid for the property.

LVR on a $500,000 Property

The LVR can vary significantly depending on the size of your home loans and your deposit, directly impacting the equity you need to borrow. Here’s a quick breakdown of how different loan amounts translate into LVRs:

| Deposit | Loan Amount | LVR |

| $25,000 | $475,000 | 95% |

| $50,000 | $450,000 | 90% |

| $75,000 | $425,000 | 85% |

| $100,000 | $400,000 | 80% |

How Lenders use LVR

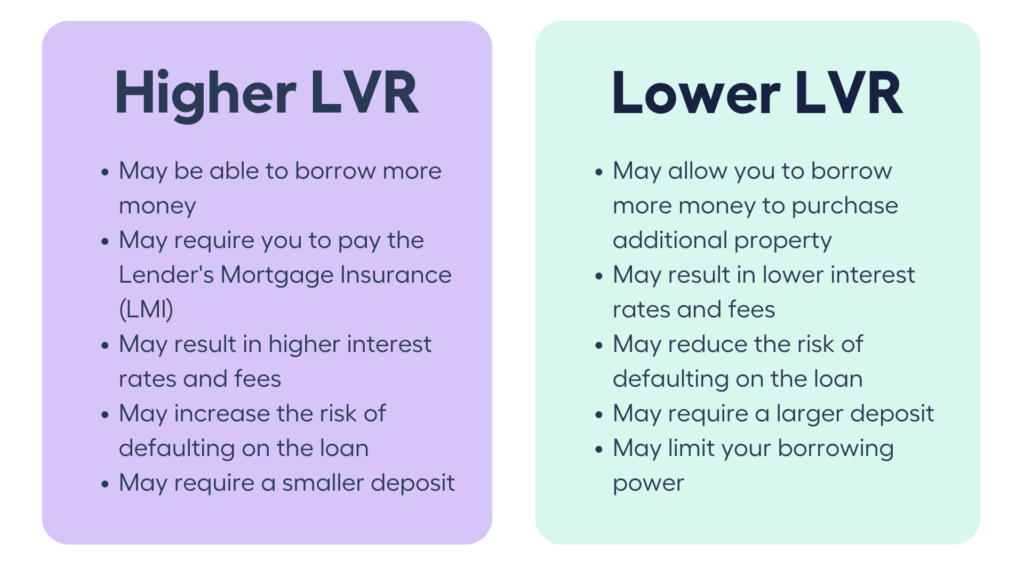

The LVR determines whether a lender will approve a mortgage application. A higher LVR means you’ve put down a smaller deposit than the property’s value, which can be a red flag for lenders. This increases the likelihood of your application being rejected.

On the other hand, a lower LVR shows that you’ve made a larger deposit, which makes you less of a risk in the lender’s eyes. As a result, it’s more likely they’ll approve your application.

Impact of LVR on Mortgage Approval

Most lenders prefer an LVR of 80% or lower to approve a loan. Why? Because it’s less risky for them. However, an LVR above 80% doesn’t mean your home loan application is rejected on the spot. It just means you’ll have to pay Lenders Mortgage Insurance (LMI) to protect the lender, which adds an extra cost to your property or purchase price. An LVR above 80% may also mean your loan is subject to stricter conditions.

How LVR Affects Borrowers

The loan-to-value ratio primarily affects you as a borrower by determining how much money you can borrow. A higher LVR means you have less equity in the total value of the property, which is a loan-to-valuation ratio that can limit the amount a bank or financial institution is willing to lend. For example, if a lender has a maximum LVR of 80%, you must provide a 20% deposit to borrow the remaining 80% of the property’s value.

Interest Rates and LVR

The LVR doesn’t just affect the amount you can borrow. Most lenders adjust interest rates based on the LVR as well. Usually, a lower LVR means a lower interest rate. Conversely, a higher LVR can lead to higher interest rates, as the lender wants to cover the extra risk. So, the lower your LVR, the bigger your deposit and the better your loan conditions will likely be.

Lenders Mortgage Insurance (LMI)

LMI is an insurance policy that protects the lender if you fail to repay your loan. It’s typically required when the LVR exceeds 80%. The cost of LMI protects the lender varies based on your loan amount and LVR; you can either pay it upfront or roll it into your loan. While LMI adds to the overall cost of your loan, it can also help you get a mortgage with a smaller deposit.

What is a Good LVR?

Generally, a good LVR is considered to be 80% or lower. Lenders view a good LVR as less risky, which can result in upfront costs and more favourable loan terms. On the other hand, an LVR higher than 80% is often seen as bad, potentially leading to higher costs and stricter lending conditions.

Real-World Examples of LVR

In Australia, LVRs commonly range from 80% to 95%, depending on factors like the lender, the loan amount, and the borrower’s financial profile. Here are a couple of real-world examples:

- First-Home Buyer: Janice, a proud first-home buyer, buys a 3-bedroom townhouse worth $629,000 (the average price for a first home in Australia). She puts down a deposit of $157,250 and borrows $471,750, resulting in an LVR of 75%. By securing a lower LVR, Janice avoids paying LMI and benefits from a lower interest rate.

- Investor: John, an investor, uses equity from his existing property to buy an apartment and expand his portfolio. He borrows $425,000, resulting in an LVR of 85%. This allows John to grow his portfolio but faces higher interest rates due to the increased risk.

4 Tips to Lower Your LVR

A low loan-to-value ratio can help you avoid paying LMI and result in lower interest rates, too – so it’s worth exploring every option to bring it down.

Here are four ways to lower your LVR:

- Increase your deposit: The more extensive your deposit, the lower your LVR. Saving more money might take extra time, but it could save you thousands of dollars through lower interest rates and no LMI.

- Help from a loved one: Family financial support can make a big difference. Whether it’s a gift towards your deposit or using a guarantor loan – where a family member, often a parent, offers their property as security – this support can lower your LVR and improve your loan terms.

- Buy a lower-priced property: Opting for a more affordable property can also reduce your LVR, making it easier to get a loan. That doesn’t mean you have to give up on your dream home. Sometimes, a smaller or less flashy option can be just as satisfying (and require less work to clean and maintain).

- Use government grants or incentives: If it’s your first home, you should look into any government grants or incentives available, such as the First Home Owner Grant (FHOG) or the First Home Guarantee (FHBG). These can provide a helpful boost to your deposit, reducing your LVR and making your loan more manageable.

LVR When Buying an Investment Property

LVR is usually higher for investment properties than homes you plan to live in. Lenders see investment properties as riskier than home loans because they rely on rental income, which can be less predictable than personal income. As you might have guessed by now, lenders don’t like risk.

Because of this, many lenders require a larger deposit (resulting in a lower LVR) for investment loans. They might also charge higher interest rates to cover the added risk. However, LVR limits can vary between lenders. Some may have a bigger deposit but still offer competitive LVRs for investment properties, especially if you have a strong financial profile.

Risks of Using High LVR for Property Investment

While a low LVR is ideal for owner-occupiers, property investors might be more comfortable with a higher LVR. This is because they can use their equity to buy additional properties and expand their portfolio more quickly. By leveraging their existing equity, they avoid the need to spend as much time saving up for a large deposit to achieve a low LVR.

The downside is that this strategy comes with risks, such as:

- Market volatility: If property values decline, your LVR could increase, putting you at risk of owing more than your property is worth. This is commonly known as “underwater” or “upside down” on a mortgage.

- Higher costs: Lenders may charge higher interest rates on loans with higher LVRs, and if your LVR rises too much, you could face additional fees or tighter lending conditions.

- Regulatory changes: Regulatory changes can also affect LVR limits, borrowing conditions, and lending criteria. If regulations tighten, securing financing or refinancing existing loans might be more challenging, especially with a higher LVR.

Conclusion

Understanding the home loan amount-to-value ratio (LVR) helps you make smarter decisions when buying a home. A lower LVR makes getting a loan easier and can lead to better terms, lower interest rates, and less financial risk.

Figuring out LVR and finding the best loan terms can be tricky, but you don’t have to do it alone. A mortgage broker can help you find great deals, explain more about how LVR works, and guide you every step of the way. Ready to take the next step? Check out the best mortgage brokers in your area from our top 10 list. You’ll find Sydney mortgage brokers, Melbourne mortgage brokers, and Brisbane mortgage brokers with incredible reviews and track records.

FAQs on Loan-To-Value Ratio (LVR)

- What is the Loan-to-Value Ratio (LVR)?

LVR, or Loan-to-Value Ratio, is a financial term that helps lenders assess the risk of a home loan. It’s determined by dividing the total loan amount by the property’s value and is expressed as a percentage.

- How is LVR calculated?

LVR is calculated using the formula:

LVR = (Loan Amount/Property Value) × 100

For example, if the loan amount is $400,000 and the property value is $500,000, the LVR would be 80%.

- Why is LVR important when applying for a home loan?

LVR is important because it helps lenders assess the risk of the loan. A lower LVR generally means lower risk for the lender, resulting in better loan terms such as lower interest rates. A higher LVR means higher risk for the lender. This means you may face higher interest rates, stricter lending conditions, or need to pay for Lender’s Mortgage Insurance (LMI).

- What is considered a good LVR?

A good LVR is 80% or lower. This amount allows you to acquire a loan without paying Lenders Mortgage Insurance (LMI) and can help you qualify for more favourable interest rates.

- What is Lenders Mortgage Insurance (LMI)?

LMI is an insurance policy that protects the lender if you fail to repay your loan. It is usually required when the LVR exceeds 80%. The cost of LMI protects the lender varies based on the loan amount and LVR.

- Can I avoid paying LMI?

You can avoid paying LMI by having an LVR of 80% of market value or lower. This means saving up for a larger deposit (at least 20%), so your loan amount is less than 80% of the property’s value.

- How does a high LVR affect my loan application?

A high LVR means a higher risk for the lender. The lender may charge you higher interest rates and LMI to offset this risk. A high LVR may also limit your loan amount and affect approval.

- What strategies can I use to lower my LVR?

To lower your LVR, consider increasing your deposit, choosing a less expensive property, borrowing or using a guarantor. These strategies can help you take less risk and achieve a lower LVR, leading to better loan conditions.

- How does the property market affect LVR?

The bank’s property valuation, purchase price and market changes can impact LVR. For example, if property values decrease, the LVR may increase, making refinancing or selling the property harder. On the other hand, rising property values can decrease the LVR, improving your equity.

- What is the typical LVR for property investors?

Property investors often have higher LVRs than home buyers, up to 90% or more. This is because they can leverage the equity from their existing properties to secure additional loans. However, due to the perceived higher risk, investors may face stricter lending criteria and higher interest rates than owner-occupiers.